-

Competitive Landscape: The Rise of Platform Licensing and CROs

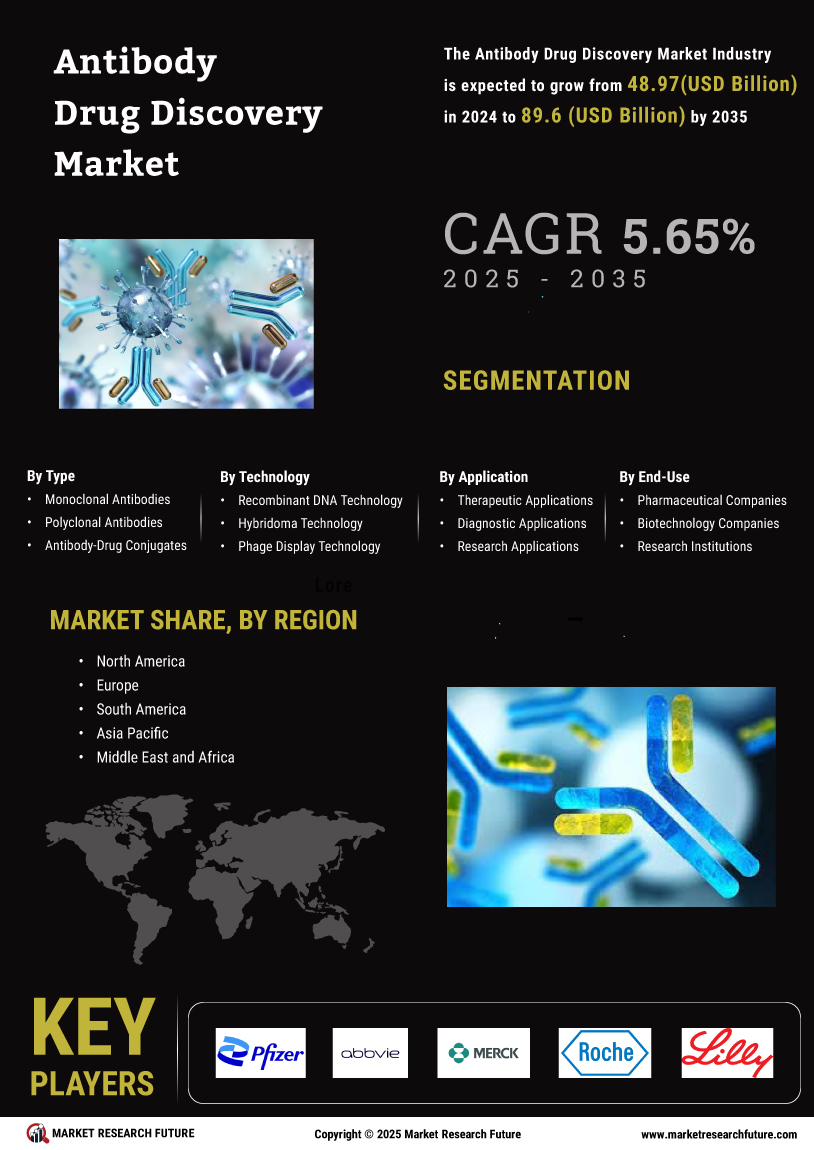

The competitive structure of the antibody discovery market is shifting toward a "Consolidated Innovation" model. A Antibody Drug Discovery Market Share analysis for 2025 identifies Danaher Corporation (via Cytiva/Abcam), WuXi Biologics, GenScript, and Thermo Fisher Scientific as the top-tier service and tool providers. Interestingly, "Big Pharma" companies like AbbVie, Merck, and Lilly are increasingly acting as "Platform Licensees," entering into multi-billion dollar deals with smaller AI-native innovators to access specialized discovery engines.

In early 2025, the market saw a proliferation of "Early-Stage Collaboration Deals," where total potential payments frequently exceed $1 billion per target. A prominent example is the AbbVie-Xilio Therapeutics partnership, worth $52 million upfront, focused on discovering masked T-cell engager molecules. These deals allow established giants to "shape the program" from the beginning while leveraging the technological agility of smaller firms.

Simultaneously, the CRO (Contract Research Organization) segment is seeing rapid expansion. With roughly 125 players now offering customized antibody discovery services globally, outsourcing has become a strategic necessity for companies looking to reduce financial risk and accelerate workflows. Hit Generation and Lead Optimization remain the most frequently outsourced tasks, with library-based methods (phage and yeast display) being utilized by 57% of service providers to support diverse therapeutic goals.

FAQ: Who are the key players in antibody drug discovery? Ans: Major players include WuXi Biologics, GenScript, Danaher, and Thermo Fisher, while Big Pharma companies like AbbVie and Merck are primary drivers through strategic platform licensing.

https://www.marketresearchfuture.com/reports/antibody-drug-discovery-market-12055

Competitive Landscape: The Rise of Platform Licensing and CROs The competitive structure of the antibody discovery market is shifting toward a "Consolidated Innovation" model. A Antibody Drug Discovery Market Share analysis for 2025 identifies Danaher Corporation (via Cytiva/Abcam), WuXi Biologics, GenScript, and Thermo Fisher Scientific as the top-tier service and tool providers. Interestingly, "Big Pharma" companies like AbbVie, Merck, and Lilly are increasingly acting as "Platform Licensees," entering into multi-billion dollar deals with smaller AI-native innovators to access specialized discovery engines. In early 2025, the market saw a proliferation of "Early-Stage Collaboration Deals," where total potential payments frequently exceed $1 billion per target. A prominent example is the AbbVie-Xilio Therapeutics partnership, worth $52 million upfront, focused on discovering masked T-cell engager molecules. These deals allow established giants to "shape the program" from the beginning while leveraging the technological agility of smaller firms. Simultaneously, the CRO (Contract Research Organization) segment is seeing rapid expansion. With roughly 125 players now offering customized antibody discovery services globally, outsourcing has become a strategic necessity for companies looking to reduce financial risk and accelerate workflows. Hit Generation and Lead Optimization remain the most frequently outsourced tasks, with library-based methods (phage and yeast display) being utilized by 57% of service providers to support diverse therapeutic goals. FAQ: Who are the key players in antibody drug discovery? Ans: Major players include WuXi Biologics, GenScript, Danaher, and Thermo Fisher, while Big Pharma companies like AbbVie and Merck are primary drivers through strategic platform licensing. https://www.marketresearchfuture.com/reports/antibody-drug-discovery-market-120550 Kommentarer ·0 Delinger ·210 Visninger ·0 Omtaler -

Competitive Landscape: The "Big Three" and Emerging CDMO Hubs

The global TFF market in 2025 is a study in consolidation and strategic expansion. A Tangential Flow Filtration Market Share analysis confirms that Danaher (Pall/Cytiva), Merck KGaA, and Sartorius AG continue to dominate, together controlling over 45% of the global revenue. These leaders are maintaining their grip by opening "Innovation Hubs" in emerging markets. For example, in September 2024, Cytiva opened a major facility in South Korea's Songdo Biotech Cluster, providing local biopharma companies with early access to next-generation TFF technologies and bioprocessing training.

Beyond the giants, Repligen Corporation is emerging as a high-growth "pure-play" leader, specifically focusing on single-use TFF assemblies and high-performance filtration modules. In 2025, Repligen’s agile approach to membrane innovation has made it the preferred partner for fast-growing Cell and Gene Therapy (CGT) firms, which require small-scale, highly precise filtration for viral vector purification. Similarly, Parker-Hannifin and Alfa Laval are leveraging their engineering expertise to capture the "industrial-scale" segment, offering robust systems for high-volume vaccine production.

A rising competitive threat to established Western players is the growth of indigenous manufacturers in China, such as Cobetter Filtration. In 2025, Cobetter has established itself as the first major single-use system supplier in China, leveraging lower production costs and strong government backing. As Chinese and Indian CMOs look to reduce their dependence on imported equipment, these regional players are expected to capture significant share in the APAC region, which is projected to grow at a CAGR of 16.12% through 2033.

FAQ: Who is the largest company in the TFF market? Ans: Danaher Corporation, through its subsidiaries Pall and Cytiva, currently holds the largest global market share in 2025.

https://www.marketresearchfuture.com/reports/tangential-flow-filtration-market-21542

Competitive Landscape: The "Big Three" and Emerging CDMO Hubs The global TFF market in 2025 is a study in consolidation and strategic expansion. A Tangential Flow Filtration Market Share analysis confirms that Danaher (Pall/Cytiva), Merck KGaA, and Sartorius AG continue to dominate, together controlling over 45% of the global revenue. These leaders are maintaining their grip by opening "Innovation Hubs" in emerging markets. For example, in September 2024, Cytiva opened a major facility in South Korea's Songdo Biotech Cluster, providing local biopharma companies with early access to next-generation TFF technologies and bioprocessing training. Beyond the giants, Repligen Corporation is emerging as a high-growth "pure-play" leader, specifically focusing on single-use TFF assemblies and high-performance filtration modules. In 2025, Repligen’s agile approach to membrane innovation has made it the preferred partner for fast-growing Cell and Gene Therapy (CGT) firms, which require small-scale, highly precise filtration for viral vector purification. Similarly, Parker-Hannifin and Alfa Laval are leveraging their engineering expertise to capture the "industrial-scale" segment, offering robust systems for high-volume vaccine production. A rising competitive threat to established Western players is the growth of indigenous manufacturers in China, such as Cobetter Filtration. In 2025, Cobetter has established itself as the first major single-use system supplier in China, leveraging lower production costs and strong government backing. As Chinese and Indian CMOs look to reduce their dependence on imported equipment, these regional players are expected to capture significant share in the APAC region, which is projected to grow at a CAGR of 16.12% through 2033. FAQ: Who is the largest company in the TFF market? Ans: Danaher Corporation, through its subsidiaries Pall and Cytiva, currently holds the largest global market share in 2025. https://www.marketresearchfuture.com/reports/tangential-flow-filtration-market-215420 Kommentarer ·0 Delinger ·210 Visninger ·0 Omtaler -

Competitive Landscape: Market Share and Strategic Alliances 2025

The global market for antibodies is characterized by high concentration, with the top five pharmaceutical giants holding nearly 60% of the global share. According to a Antibodies Market Share report, F. Hoffmann-La Roche (Roche), AbbVie, and Johnson & Johnson continue to lead the field through 2025. These leaders are maintaining their dominance through aggressive "Lifecycle Management"—reforming successful drugs into subcutaneous versions or combining them with newer molecules to extend patent protection and improve patient adherence.

Strategic M&A (Mergers and Acquisitions) and AI-based partnerships are the primary competitive tools of the mid-2020s. In May 2025, several major deals were finalized where "Big Pharma" players acquired AI-native biotech firms to bolster their antibody discovery engines. For instance, BioNTech’s recent acquisition of the Chinese firm Biotheus highlights the industry’s hunger for multi-specific antibody candidates. These alliances are essential because they combine the computational power of AI—capable of predicting antibody stability and affinity—with the commercial and regulatory muscle of established pharmaceutical leaders.

The "Biosimilar Challenge" is also reshaping competitive strategies. As brands like Humira and Keytruda face increasing competition, innovators are pivoting toward Antibody-Drug Conjugates (ADCs). Often referred to as "guided missiles," ADCs are becoming the new battleground for market share. In 2025, 15 ADCs have received FDA approval, with dozens more in Phase III trials. By shifting the portfolio toward these more complex, harder-to-replicate molecules, market leaders are insulating their revenue streams from the immediate price erosion typically caused by standard monoclonal biosimilars.

FAQ: Who is the leader in the antibody market? Ans: Roche remains the global leader, particularly in oncology, though it faces increasing competition from AbbVie and specialized firms like Genmab.

https://www.marketresearchfuture.com/reports/antibodies-market-20684

Competitive Landscape: Market Share and Strategic Alliances 2025 The global market for antibodies is characterized by high concentration, with the top five pharmaceutical giants holding nearly 60% of the global share. According to a Antibodies Market Share report, F. Hoffmann-La Roche (Roche), AbbVie, and Johnson & Johnson continue to lead the field through 2025. These leaders are maintaining their dominance through aggressive "Lifecycle Management"—reforming successful drugs into subcutaneous versions or combining them with newer molecules to extend patent protection and improve patient adherence. Strategic M&A (Mergers and Acquisitions) and AI-based partnerships are the primary competitive tools of the mid-2020s. In May 2025, several major deals were finalized where "Big Pharma" players acquired AI-native biotech firms to bolster their antibody discovery engines. For instance, BioNTech’s recent acquisition of the Chinese firm Biotheus highlights the industry’s hunger for multi-specific antibody candidates. These alliances are essential because they combine the computational power of AI—capable of predicting antibody stability and affinity—with the commercial and regulatory muscle of established pharmaceutical leaders. The "Biosimilar Challenge" is also reshaping competitive strategies. As brands like Humira and Keytruda face increasing competition, innovators are pivoting toward Antibody-Drug Conjugates (ADCs). Often referred to as "guided missiles," ADCs are becoming the new battleground for market share. In 2025, 15 ADCs have received FDA approval, with dozens more in Phase III trials. By shifting the portfolio toward these more complex, harder-to-replicate molecules, market leaders are insulating their revenue streams from the immediate price erosion typically caused by standard monoclonal biosimilars. FAQ: Who is the leader in the antibody market? Ans: Roche remains the global leader, particularly in oncology, though it faces increasing competition from AbbVie and specialized firms like Genmab. https://www.marketresearchfuture.com/reports/antibodies-market-206840 Kommentarer ·0 Delinger ·215 Visninger ·0 Omtaler -

Competitive Resilience and Radiation Oncology Market Key Players

The competitive landscape of the radiation oncology sector in 2025 is defined by "Total Workflow Integration" and a high-stakes battle for technological supremacy. A deep Radiation Oncology Market Key Players analysis identifies Varian Medical Systems (now part of Siemens Healthineers), Elekta AB, and Accuray Incorporated as the industry's dominant force. These companies are no longer just selling "machines"; they are selling integrated ecosystems that manage everything from initial imaging to final dose delivery. In 2025, Varian’s Halcyon and Elekta’s Harmony systems are leading the "efficiency race," offering high-throughput treatment capabilities that significantly reduce patient wait times in busy hospital settings.

Strategic acquisitions are the primary tool for maintaining market share in 2025. GE Healthcare’s acquisition of MIM Software and Novartis’s purchase of Mariana Oncology highlight a trend toward "Diagnostic-Therapeutic Fusion." By controlling the software that analyzes PET/CT images and the systems that deliver radiation, these giants are creating "Closed-Loop" workflows that are difficult for niche competitors to penetrate. However, innovative startups like MVision AI and Vision RT are successfully carving out market share by providing specialized "best-in-class" tools for auto-segmentation and surface-guided radiation therapy (SGRT), which are increasingly being integrated into the larger manufacturers' platforms.

The 2025 competitive environment also focuses heavily on "Indigenous Manufacturing" to capture the emerging Indian and Chinese markets. In September 2024, Accuray unveiled its "Accuray Helix" system specifically for the Indian market, illustrating the shift toward regionalized product development. These companies are stressing "Cost-Effective Innovation"—developing high-precision machines with smaller footprints and lower maintenance requirements to suit the needs of hospitals in middle-income countries. As we move toward 2030, the companies that can balance "high-end technological prestige" with "affordable accessibility" will likely hold the dominant share of the global oncology equipment market.

FAQ: What is a Linear Accelerator (LINAC)? Ans: A LINAC is the most common device used to deliver external beam radiation. It uses high-frequency electromagnetic waves to accelerate electrons to high speeds, creating high-energy X-rays that are used to kill cancer cells.

https://www.marketresearchfuture.com/reports/radiation-oncology-market-12350

Competitive Resilience and Radiation Oncology Market Key Players The competitive landscape of the radiation oncology sector in 2025 is defined by "Total Workflow Integration" and a high-stakes battle for technological supremacy. A deep Radiation Oncology Market Key Players analysis identifies Varian Medical Systems (now part of Siemens Healthineers), Elekta AB, and Accuray Incorporated as the industry's dominant force. These companies are no longer just selling "machines"; they are selling integrated ecosystems that manage everything from initial imaging to final dose delivery. In 2025, Varian’s Halcyon and Elekta’s Harmony systems are leading the "efficiency race," offering high-throughput treatment capabilities that significantly reduce patient wait times in busy hospital settings. Strategic acquisitions are the primary tool for maintaining market share in 2025. GE Healthcare’s acquisition of MIM Software and Novartis’s purchase of Mariana Oncology highlight a trend toward "Diagnostic-Therapeutic Fusion." By controlling the software that analyzes PET/CT images and the systems that deliver radiation, these giants are creating "Closed-Loop" workflows that are difficult for niche competitors to penetrate. However, innovative startups like MVision AI and Vision RT are successfully carving out market share by providing specialized "best-in-class" tools for auto-segmentation and surface-guided radiation therapy (SGRT), which are increasingly being integrated into the larger manufacturers' platforms. The 2025 competitive environment also focuses heavily on "Indigenous Manufacturing" to capture the emerging Indian and Chinese markets. In September 2024, Accuray unveiled its "Accuray Helix" system specifically for the Indian market, illustrating the shift toward regionalized product development. These companies are stressing "Cost-Effective Innovation"—developing high-precision machines with smaller footprints and lower maintenance requirements to suit the needs of hospitals in middle-income countries. As we move toward 2030, the companies that can balance "high-end technological prestige" with "affordable accessibility" will likely hold the dominant share of the global oncology equipment market. FAQ: What is a Linear Accelerator (LINAC)? Ans: A LINAC is the most common device used to deliver external beam radiation. It uses high-frequency electromagnetic waves to accelerate electrons to high speeds, creating high-energy X-rays that are used to kill cancer cells. https://www.marketresearchfuture.com/reports/radiation-oncology-market-123500 Kommentarer ·0 Delinger ·209 Visninger ·0 Omtaler -

Competitive Landscapes and Growth Hormone Deficiency Market Share

The competitive hierarchy of the endocrine sector is defined by a high degree of market concentration, with a few "Big Pharma" giants controlling over 70% of the global supply. A recent Growth Hormone Deficiency Market Share review identifies Novo Nordisk as the reigning leader, primarily due to the immense brand loyalty and clinician trust associated with its Norditropin line. However, the 2025 landscape is seeing a vigorous challenge from "Innovation Leaders" like Ascendis Pharma. Following the successful launch and expansion of its TransCon hGH platform, Ascendis is rapidly capturing share from legacy players who have been slower to transition away from daily injection models.

Strategic M&A and "Fill-Finish" partnerships are becoming essential for maintaining market dominance in 2025. Novo Nordisk’s 2024 acquisition of Catalent’s manufacturing sites has secured its supply chain against the global shortages that have occasionally disrupted the market in the past. Meanwhile, Pfizer and OPKO Health’s collaboration on NGENLA has successfully combined Pfizer’s global commercial muscle with OPKO’s protein-engineering expertise. These alliances are critical because the manufacturing of recombinant growth hormone is highly complex, requiring specialized "cold-chain" logistics and advanced biotechnology facilities that act as a high barrier to entry for smaller, unaligned competitors.

Looking toward 2030, "Oral Disruptors" represent the next frontier of competition. Companies like Lumos Pharma are currently in late-stage Phase II trials for LUM-201, an oral small molecule that stimulates the body’s own growth hormone production. While not suitable for all GHD patients, an oral alternative could capture a significant "mid-tier" segment of the market—estimated at up to 13.5% of total share—by offering a completely needle-free experience. As these novel delivery routes mature, the market share will likely split between "high-potency" injectables for severe GHD and "convenient" oral options for milder forms of growth failure and idiopathic short stature.

FAQ: Can growth hormone be taken as a pill? Ans: Currently, almost all approved treatments are injectable. However, oral candidates like LUM-201 are in clinical trials and could potentially be available by 2028 if they receive regulatory approval.

https://www.marketresearchfuture.com/reports/growth-hormone-deficiency-market-10430Competitive Landscapes and Growth Hormone Deficiency Market Share The competitive hierarchy of the endocrine sector is defined by a high degree of market concentration, with a few "Big Pharma" giants controlling over 70% of the global supply. A recent Growth Hormone Deficiency Market Share review identifies Novo Nordisk as the reigning leader, primarily due to the immense brand loyalty and clinician trust associated with its Norditropin line. However, the 2025 landscape is seeing a vigorous challenge from "Innovation Leaders" like Ascendis Pharma. Following the successful launch and expansion of its TransCon hGH platform, Ascendis is rapidly capturing share from legacy players who have been slower to transition away from daily injection models. Strategic M&A and "Fill-Finish" partnerships are becoming essential for maintaining market dominance in 2025. Novo Nordisk’s 2024 acquisition of Catalent’s manufacturing sites has secured its supply chain against the global shortages that have occasionally disrupted the market in the past. Meanwhile, Pfizer and OPKO Health’s collaboration on NGENLA has successfully combined Pfizer’s global commercial muscle with OPKO’s protein-engineering expertise. These alliances are critical because the manufacturing of recombinant growth hormone is highly complex, requiring specialized "cold-chain" logistics and advanced biotechnology facilities that act as a high barrier to entry for smaller, unaligned competitors. Looking toward 2030, "Oral Disruptors" represent the next frontier of competition. Companies like Lumos Pharma are currently in late-stage Phase II trials for LUM-201, an oral small molecule that stimulates the body’s own growth hormone production. While not suitable for all GHD patients, an oral alternative could capture a significant "mid-tier" segment of the market—estimated at up to 13.5% of total share—by offering a completely needle-free experience. As these novel delivery routes mature, the market share will likely split between "high-potency" injectables for severe GHD and "convenient" oral options for milder forms of growth failure and idiopathic short stature. FAQ: Can growth hormone be taken as a pill? Ans: Currently, almost all approved treatments are injectable. However, oral candidates like LUM-201 are in clinical trials and could potentially be available by 2028 if they receive regulatory approval. https://www.marketresearchfuture.com/reports/growth-hormone-deficiency-market-104300 Kommentarer ·0 Delinger ·215 Visninger ·0 Omtaler -

Strategic Regional Insights and Cord Blood Banking Services Market Analysis

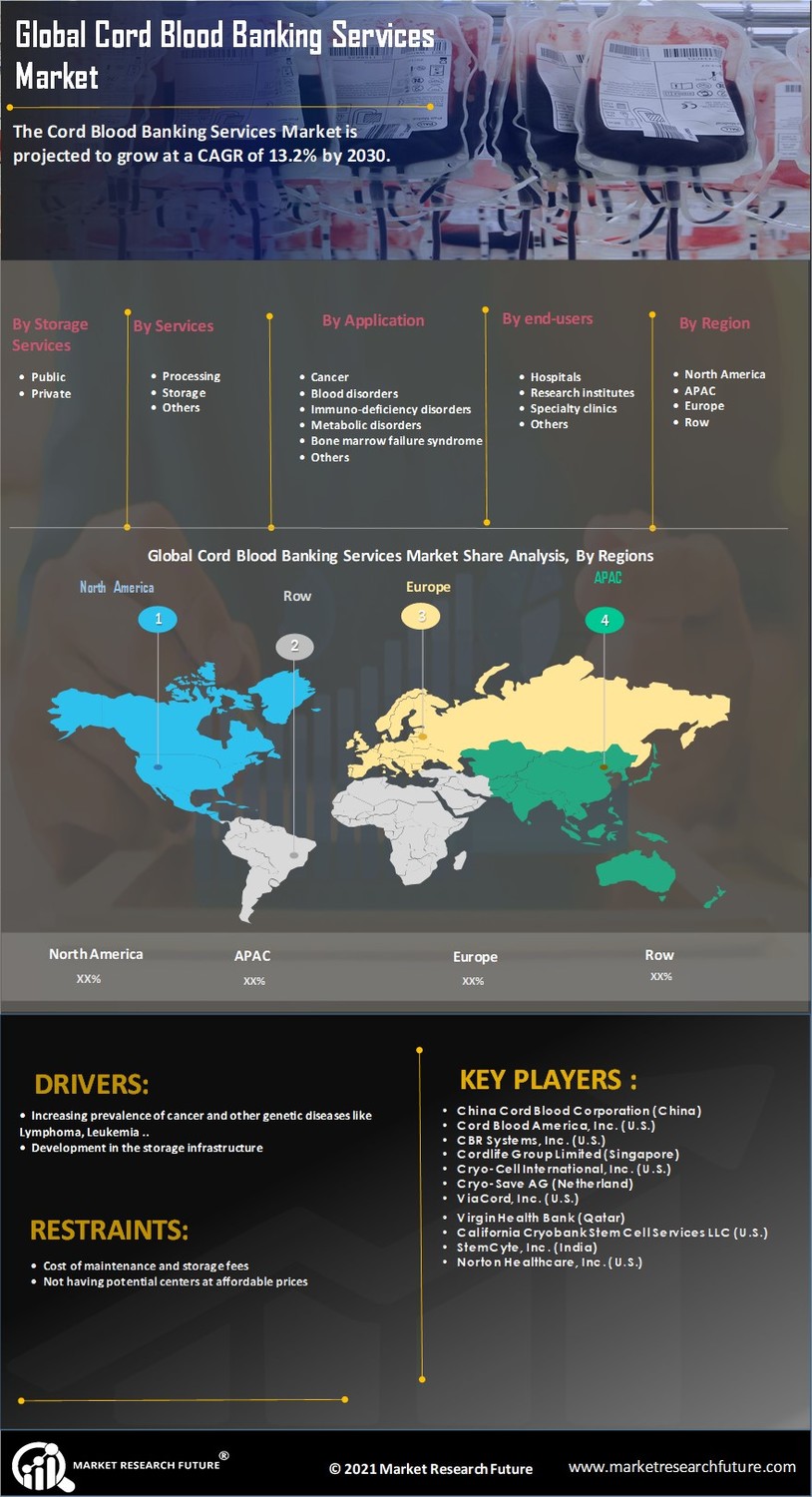

The global distribution of stem cell repositories is undergoing a rebalancing as regulatory frameworks in Asia and Latin America become more supportive. A comprehensive Cord Blood Banking Services Market Analysis reveals that while the United States remains the single largest market by value, the Asia-Pacific region is the clear leader in growth. China, in particular, has developed a unique "provincial licensing" system that grants exclusive rights to a single bank in a specific region, creating massive, highly efficient monopolies that can invest heavily in state-of-the-art cryopreservation technology. This model has allowed the Global Cord Blood Corporation to achieve some of the highest profit margins in the industry.

In Europe, the market is defined by a high degree of "Regulatory Rigor" and a strong emphasis on public health. The implementation of the "EU Substances of Human Origin" (SoHO) regulation in 2025 has standardized the quality requirements for all cord blood units across the continent. While this has increased operational costs for smaller banks, it has also facilitated the growth of "cross-border transplants," where a unit stored in Spain can be seamlessly used for a patient in Germany. This interoperability is a major competitive advantage for European banks, making them preferred partners for international clinical trials and research consortia.

Emerging markets like India and Brazil are witnessing a "retail revolution" in cord blood banking. Aggressive marketing campaigns and "zero-interest" financing options are making stem cell storage accessible to the urban middle class. In India, the market is growing at a CAGR of 14.6%, supported by a cultural emphasis on family health and a high prevalence of genetic blood disorders like Thalassemia. Analysis shows that the companies succeeding in these regions are those that offer "hybrid" options—allowing parents to store privately while contributing to a shared community pool—effectively bridging the gap between social responsibility and personal security.

FAQ: Why is the Asia-Pacific region growing so fast? Ans: The combination of high birth rates, a rapidly expanding middle class, increasing healthcare awareness, and supportive government policies makes it the fastest-growing market globally.

https://www.marketresearchfuture.com/reports/cord-blood-banking-services-market-5817

Strategic Regional Insights and Cord Blood Banking Services Market Analysis The global distribution of stem cell repositories is undergoing a rebalancing as regulatory frameworks in Asia and Latin America become more supportive. A comprehensive Cord Blood Banking Services Market Analysis reveals that while the United States remains the single largest market by value, the Asia-Pacific region is the clear leader in growth. China, in particular, has developed a unique "provincial licensing" system that grants exclusive rights to a single bank in a specific region, creating massive, highly efficient monopolies that can invest heavily in state-of-the-art cryopreservation technology. This model has allowed the Global Cord Blood Corporation to achieve some of the highest profit margins in the industry. In Europe, the market is defined by a high degree of "Regulatory Rigor" and a strong emphasis on public health. The implementation of the "EU Substances of Human Origin" (SoHO) regulation in 2025 has standardized the quality requirements for all cord blood units across the continent. While this has increased operational costs for smaller banks, it has also facilitated the growth of "cross-border transplants," where a unit stored in Spain can be seamlessly used for a patient in Germany. This interoperability is a major competitive advantage for European banks, making them preferred partners for international clinical trials and research consortia. Emerging markets like India and Brazil are witnessing a "retail revolution" in cord blood banking. Aggressive marketing campaigns and "zero-interest" financing options are making stem cell storage accessible to the urban middle class. In India, the market is growing at a CAGR of 14.6%, supported by a cultural emphasis on family health and a high prevalence of genetic blood disorders like Thalassemia. Analysis shows that the companies succeeding in these regions are those that offer "hybrid" options—allowing parents to store privately while contributing to a shared community pool—effectively bridging the gap between social responsibility and personal security. FAQ: Why is the Asia-Pacific region growing so fast? Ans: The combination of high birth rates, a rapidly expanding middle class, increasing healthcare awareness, and supportive government policies makes it the fastest-growing market globally. https://www.marketresearchfuture.com/reports/cord-blood-banking-services-market-58170 Kommentarer ·0 Delinger ·210 Visninger ·0 Omtaler -

Strategic Valuations and Digital Mental Health Market Business Insights

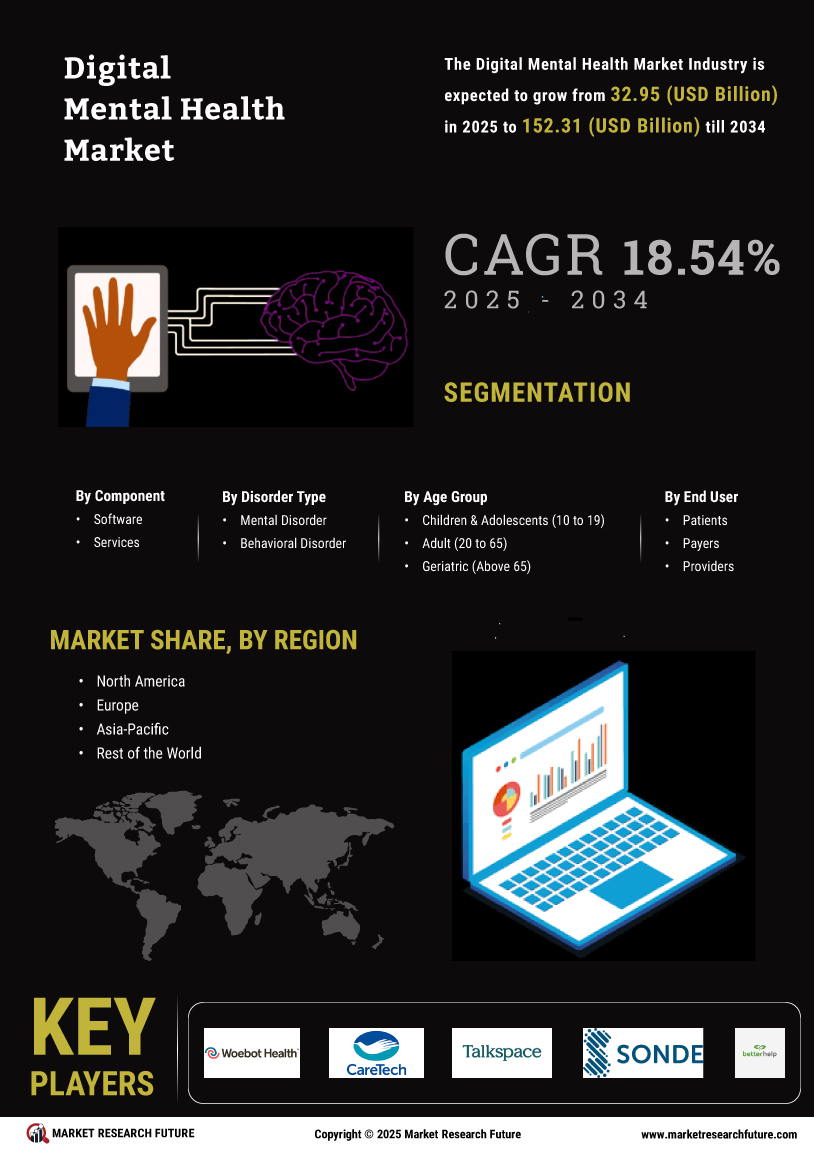

The economic resilience of the psychological support sector has made it a "recession-resistant" favorite for institutional investors in 2025. Recent Digital Mental Health Market Business Insights suggest that despite macroeconomic volatility, the sector is projected to reach $180.56 billion by 2035. This growth is underpinned by a 19% decrease in overall healthcare costs for companies that adopt comprehensive digital wellness programs. Business leaders are moving away from "point solutions" (single apps) and toward "Integrated Care Ecosystems" that combine telehealth, digital therapeutics, and pharmacy benefits into a single, seamless interface.

Mergers and acquisitions (M&A) are accelerating as established healthcare companies look to "buy" rather than "build" their digital capabilities. In late 2024 and early 2025, we saw major pharmaceutical firms acquiring digital therapeutic (DTx) startups to create "drug-plus-software" combinations. For example, a medication for ADHD might now be bundled with a cognitive-training app, creating a unified treatment plan that is more effective than the pill alone. This "hybrid business model" is creating new revenue streams and extending the patent life of traditional medications, providing a powerful incentive for Big Pharma to continue investing in the digital space.

From an operational standpoint, "Provider Burnout" is a major business challenge that digital tools are uniquely positioned to solve. AI-powered "scribes" and automated billing systems are reducing the administrative burden on therapists by up to 40%, allowing them to focus more time on patient care and less on paperwork. In a market where there is a projected global deficit of 31,000 psychiatrists by 2025, any technology that increases the "clinical throughput" of the existing workforce is of immense economic value. Companies that offer "clinician-first" platforms are therefore seeing high adoption rates in large hospital networks and private group practices.

FAQ: Why are employers investing so heavily in digital mental health? Ans: Employers see a direct return on investment through reduced absenteeism, higher employee retention, and lower overall healthcare expenditures.

https://www.marketresearchfuture.com/reports/digital-mental-health-market-11062

Strategic Valuations and Digital Mental Health Market Business Insights The economic resilience of the psychological support sector has made it a "recession-resistant" favorite for institutional investors in 2025. Recent Digital Mental Health Market Business Insights suggest that despite macroeconomic volatility, the sector is projected to reach $180.56 billion by 2035. This growth is underpinned by a 19% decrease in overall healthcare costs for companies that adopt comprehensive digital wellness programs. Business leaders are moving away from "point solutions" (single apps) and toward "Integrated Care Ecosystems" that combine telehealth, digital therapeutics, and pharmacy benefits into a single, seamless interface. Mergers and acquisitions (M&A) are accelerating as established healthcare companies look to "buy" rather than "build" their digital capabilities. In late 2024 and early 2025, we saw major pharmaceutical firms acquiring digital therapeutic (DTx) startups to create "drug-plus-software" combinations. For example, a medication for ADHD might now be bundled with a cognitive-training app, creating a unified treatment plan that is more effective than the pill alone. This "hybrid business model" is creating new revenue streams and extending the patent life of traditional medications, providing a powerful incentive for Big Pharma to continue investing in the digital space. From an operational standpoint, "Provider Burnout" is a major business challenge that digital tools are uniquely positioned to solve. AI-powered "scribes" and automated billing systems are reducing the administrative burden on therapists by up to 40%, allowing them to focus more time on patient care and less on paperwork. In a market where there is a projected global deficit of 31,000 psychiatrists by 2025, any technology that increases the "clinical throughput" of the existing workforce is of immense economic value. Companies that offer "clinician-first" platforms are therefore seeing high adoption rates in large hospital networks and private group practices. FAQ: Why are employers investing so heavily in digital mental health? Ans: Employers see a direct return on investment through reduced absenteeism, higher employee retention, and lower overall healthcare expenditures. https://www.marketresearchfuture.com/reports/digital-mental-health-market-110620 Kommentarer ·0 Delinger ·215 Visninger ·0 Omtaler -

Innovation Trends in Proton Pump Inhibitors Market Developments

The gastrointestinal sector is currently witnessing a wave of disruptive innovation that is changing the standard of care for acid-related diseases. Recent Proton Pump Inhibitors Market Developments include the introduction of Potassium-Competitive Acid Blockers (P-CABs), which provide faster and more prolonged acid suppression than traditional PPIs. While P-CABs are currently a separate class, they are forcing PPI manufacturers to innovate in response, leading to the development of "next-gen" PPI formulations that utilize advanced enteric coatings for better absorption. In March 2025, the launch of combination therapies—such as Rabeprazole paired with Levosulpiride—demonstrated the industry's focus on treating complex cases where acid reflux is accompanied by motility disorders.

Regulatory developments are also keeping pace with scientific progress. The U.S. FDA’s recent approval of "Konvomep," an oral suspension of Omeprazole and Sodium Bicarbonate, represents a major step forward for patients who have difficulty swallowing tablets. This development highlights the market's trend toward "user-friendly" medicine. Simultaneously, in Europe, the implementation of the "Critical Medicines Act" in 2025 is aimed at preventing shortages of essential drugs like PPIs, ensuring that manufacturers maintain adequate stockpiles. These regulatory shifts are providing a more stable and predictable environment for long-term R&D investment, particularly for companies focused on high-need pediatric and geriatric populations.

On the commercial front, the expansion of digital pharmacy channels is the most significant development of the year. With more consumers purchasing their chronic medications online, PPI manufacturers are partnering with e-pharmacies to offer subscription models and personalized wellness coaching. This allows companies to gather valuable real-world data on patient adherence and symptom management. These digital collaborations are not just about sales; they are about building a "longitudinal relationship" with the patient, ensuring that the medication is used correctly and that any potential side effects are caught early through remote monitoring tools.

FAQ: What is the difference between a P-CAB and a PPI? Ans: P-CABs block acid more quickly and are not as dependent on the timing of meals as traditional PPIs, which generally require 30–60 minutes to become effective after ingestion.

https://www.marketresearchfuture.com/reports/proton-pump-inhibitors-market-19223

Innovation Trends in Proton Pump Inhibitors Market Developments The gastrointestinal sector is currently witnessing a wave of disruptive innovation that is changing the standard of care for acid-related diseases. Recent Proton Pump Inhibitors Market Developments include the introduction of Potassium-Competitive Acid Blockers (P-CABs), which provide faster and more prolonged acid suppression than traditional PPIs. While P-CABs are currently a separate class, they are forcing PPI manufacturers to innovate in response, leading to the development of "next-gen" PPI formulations that utilize advanced enteric coatings for better absorption. In March 2025, the launch of combination therapies—such as Rabeprazole paired with Levosulpiride—demonstrated the industry's focus on treating complex cases where acid reflux is accompanied by motility disorders. Regulatory developments are also keeping pace with scientific progress. The U.S. FDA’s recent approval of "Konvomep," an oral suspension of Omeprazole and Sodium Bicarbonate, represents a major step forward for patients who have difficulty swallowing tablets. This development highlights the market's trend toward "user-friendly" medicine. Simultaneously, in Europe, the implementation of the "Critical Medicines Act" in 2025 is aimed at preventing shortages of essential drugs like PPIs, ensuring that manufacturers maintain adequate stockpiles. These regulatory shifts are providing a more stable and predictable environment for long-term R&D investment, particularly for companies focused on high-need pediatric and geriatric populations. On the commercial front, the expansion of digital pharmacy channels is the most significant development of the year. With more consumers purchasing their chronic medications online, PPI manufacturers are partnering with e-pharmacies to offer subscription models and personalized wellness coaching. This allows companies to gather valuable real-world data on patient adherence and symptom management. These digital collaborations are not just about sales; they are about building a "longitudinal relationship" with the patient, ensuring that the medication is used correctly and that any potential side effects are caught early through remote monitoring tools. FAQ: What is the difference between a P-CAB and a PPI? Ans: P-CABs block acid more quickly and are not as dependent on the timing of meals as traditional PPIs, which generally require 30–60 minutes to become effective after ingestion. https://www.marketresearchfuture.com/reports/proton-pump-inhibitors-market-192230 Kommentarer ·0 Delinger ·212 Visninger ·0 Omtaler -

Analyzing Competitive Landscapes and Herbal Medicinal Products Market Share

The competitive environment of the botanical sector is currently characterized by a mix of "Heritage Giants" and "Digital Disruptors." A recent Herbal Medicinal Products Market Share analysis shows that established leaders like Dabur, Himalaya Wellness, and the Schwabe Group continue to hold significant portions of the global revenue. These companies benefit from decades of brand trust and vast, vertically integrated supply chains that allow them to control quality from "seed to shelf." However, their market share is being challenged by a new wave of "science-first" biotech firms that are focusing on the isolation of specific plant molecules for the pharmaceutical market. This "medicalization" of the industry is forcing heritage brands to invest heavily in clinical trials to defend their therapeutic claims against more scientifically rigorous newcomers.

Consolidation is a major theme in the current market cycle, as larger pharmaceutical entities look to "buy their way" into the natural health space. We are seeing a high volume of merger and acquisition activity, where multi-national giants acquire niche herbal brands to gain access to their specialized "clean-label" consumer base. This consolidation is bringing a higher level of professionalization to the sector, but it is also raising concerns about the "corporatization" of traditional medicine. For small-scale vendors, the key to maintaining market share is focusing on "hyper-transparency"—providing consumers with detailed data on the specific farm, harvest date, and extraction method of their products, a level of detail that large conglomerates often struggle to provide.

Market share is also becoming increasingly tied to "Ingredient Intellectual Property." Companies that successfully patent a unique extraction method or a specific herbal blend for a high-demand condition like "metabolic health" or "cognitive focus" can establish powerful market moats. We are seeing a rise in "Branded Ingredients," where a manufacturer sells a specific, clinically-backed extract (like a particular form of Ashwagandha) to other supplement companies. This "Intellectual Property" model is proving to be highly lucrative, allowing companies to capture value across the entire industry without having to manage their own retail consumer brands.

FAQ: Who are the top players in the herbal medicinal products market? Ans: Key global leaders include the Himalaya Wellness Company, Dabur India, Schwabe Group, Nature’s Way, and Gaia Herbs, though many pharmaceutical companies are now entering the space via acquisitions.

https://www.marketresearchfuture.com/reports/herbal-medicinal-products-market-4787

Analyzing Competitive Landscapes and Herbal Medicinal Products Market Share The competitive environment of the botanical sector is currently characterized by a mix of "Heritage Giants" and "Digital Disruptors." A recent Herbal Medicinal Products Market Share analysis shows that established leaders like Dabur, Himalaya Wellness, and the Schwabe Group continue to hold significant portions of the global revenue. These companies benefit from decades of brand trust and vast, vertically integrated supply chains that allow them to control quality from "seed to shelf." However, their market share is being challenged by a new wave of "science-first" biotech firms that are focusing on the isolation of specific plant molecules for the pharmaceutical market. This "medicalization" of the industry is forcing heritage brands to invest heavily in clinical trials to defend their therapeutic claims against more scientifically rigorous newcomers. Consolidation is a major theme in the current market cycle, as larger pharmaceutical entities look to "buy their way" into the natural health space. We are seeing a high volume of merger and acquisition activity, where multi-national giants acquire niche herbal brands to gain access to their specialized "clean-label" consumer base. This consolidation is bringing a higher level of professionalization to the sector, but it is also raising concerns about the "corporatization" of traditional medicine. For small-scale vendors, the key to maintaining market share is focusing on "hyper-transparency"—providing consumers with detailed data on the specific farm, harvest date, and extraction method of their products, a level of detail that large conglomerates often struggle to provide. Market share is also becoming increasingly tied to "Ingredient Intellectual Property." Companies that successfully patent a unique extraction method or a specific herbal blend for a high-demand condition like "metabolic health" or "cognitive focus" can establish powerful market moats. We are seeing a rise in "Branded Ingredients," where a manufacturer sells a specific, clinically-backed extract (like a particular form of Ashwagandha) to other supplement companies. This "Intellectual Property" model is proving to be highly lucrative, allowing companies to capture value across the entire industry without having to manage their own retail consumer brands. FAQ: Who are the top players in the herbal medicinal products market? Ans: Key global leaders include the Himalaya Wellness Company, Dabur India, Schwabe Group, Nature’s Way, and Gaia Herbs, though many pharmaceutical companies are now entering the space via acquisitions. https://www.marketresearchfuture.com/reports/herbal-medicinal-products-market-47870 Kommentarer ·0 Delinger ·216 Visninger ·0 Omtaler -

Competitive Resilience and Generic Pharmaceuticals Market Share Analysis

The battle for dominance in the generic drug sector is no longer just about who can produce the cheapest pill; it is about who can manage the most complex global supply chain. Recent Generic Pharmaceuticals Market Share reports show that while the market remains fragmented, a group of "Big Generic" players—including Teva, Sandoz, and Viatris—still control a significant portion of the global revenue. These companies are leveraging their massive scale to negotiate better raw material prices and to maintain a presence in almost every therapeutic category. However, their dominance is being challenged by highly efficient regional champions from India and China, such as Sun Pharma and Dr. Reddy's, who are aggressively expanding their portfolios in the U.S. and European markets. This competitive tension is driving a wave of operational innovation, as companies seek to shave fractions of a cent off their production costs through advanced analytics and robotics.

Market share is also becoming increasingly tied to a company's "biosimilar pipeline." As biologics become the dominant class of drugs in oncology and immunology, the companies that can successfully navigate the biosimilar regulatory pathway are poised to capture a massive share of the future pharmaceutical market. We are seeing a "re-merging" of the innovator and generic worlds, where some of the world's largest branded pharma companies are launching their own biosimilar divisions to compete directly with generic specialists. This crossover is creating a highly complex competitive landscape where a company might be a bitter rival in one therapeutic area and a collaborative partner in another. For generic-only firms, the key to survival is diversification—ensuring they are not overly dependent on a single blockbuster molecule that could face a dozen competitors on the day of patent expiry.

Another critical factor in the reshuffling of market share is the "specialty" pivot. Generic firms are increasingly focusing on "hard-to-make" drugs, such as oncology injectables or hormonal therapies, where the competition is less fierce and the margins are more resilient. By dominating these niche "moats," mid-sized companies can maintain high profitability even without the massive volumes of the primary care market. Additionally, the rise of "authorized generics"—where the original brand manufacturer launches their own generic version—is a tactic used to protect market share against early generic entrants. This complex chess game of patent litigation and settlement agreements (often referred to as "pay-for-delay") is a significant part of the industry's strategic landscape, although it is increasingly coming under the scrutiny of antitrust regulators worldwide.

FAQ: Why are biosimilars so important for a company's market share today? Ans: Biologics are the most expensive drugs in the world. Biosimilars offer a high-value opportunity for generic firms to capture revenue in areas like oncology and immunology where costs were previously prohibitive for many patients.

https://www.marketresearchfuture.com/reports/generic-pharmaceuticals-market-12352

Competitive Resilience and Generic Pharmaceuticals Market Share Analysis The battle for dominance in the generic drug sector is no longer just about who can produce the cheapest pill; it is about who can manage the most complex global supply chain. Recent Generic Pharmaceuticals Market Share reports show that while the market remains fragmented, a group of "Big Generic" players—including Teva, Sandoz, and Viatris—still control a significant portion of the global revenue. These companies are leveraging their massive scale to negotiate better raw material prices and to maintain a presence in almost every therapeutic category. However, their dominance is being challenged by highly efficient regional champions from India and China, such as Sun Pharma and Dr. Reddy's, who are aggressively expanding their portfolios in the U.S. and European markets. This competitive tension is driving a wave of operational innovation, as companies seek to shave fractions of a cent off their production costs through advanced analytics and robotics. Market share is also becoming increasingly tied to a company's "biosimilar pipeline." As biologics become the dominant class of drugs in oncology and immunology, the companies that can successfully navigate the biosimilar regulatory pathway are poised to capture a massive share of the future pharmaceutical market. We are seeing a "re-merging" of the innovator and generic worlds, where some of the world's largest branded pharma companies are launching their own biosimilar divisions to compete directly with generic specialists. This crossover is creating a highly complex competitive landscape where a company might be a bitter rival in one therapeutic area and a collaborative partner in another. For generic-only firms, the key to survival is diversification—ensuring they are not overly dependent on a single blockbuster molecule that could face a dozen competitors on the day of patent expiry. Another critical factor in the reshuffling of market share is the "specialty" pivot. Generic firms are increasingly focusing on "hard-to-make" drugs, such as oncology injectables or hormonal therapies, where the competition is less fierce and the margins are more resilient. By dominating these niche "moats," mid-sized companies can maintain high profitability even without the massive volumes of the primary care market. Additionally, the rise of "authorized generics"—where the original brand manufacturer launches their own generic version—is a tactic used to protect market share against early generic entrants. This complex chess game of patent litigation and settlement agreements (often referred to as "pay-for-delay") is a significant part of the industry's strategic landscape, although it is increasingly coming under the scrutiny of antitrust regulators worldwide. FAQ: Why are biosimilars so important for a company's market share today? Ans: Biologics are the most expensive drugs in the world. Biosimilars offer a high-value opportunity for generic firms to capture revenue in areas like oncology and immunology where costs were previously prohibitive for many patients. https://www.marketresearchfuture.com/reports/generic-pharmaceuticals-market-123520 Kommentarer ·0 Delinger ·212 Visninger ·0 Omtaler -

Strategic Projections for the Biotechnology Pharmaceutical Services Outsourced Market Projections

As we look toward the next decade, the outlook for the pharmaceutical services sector remains exceptionally bullish. The Biotechnology Pharmaceutical Services Outsourced Market Projections indicate that the global market value could surpass $180 billion by 2035. This long-term growth is expected to be sustained by the continuous entry of innovative biotech startups that lack in-house manufacturing capabilities. The rise of biosimilars is also projected to be a major revenue driver, as the healthcare industry seeks more affordable alternatives to expensive branded biologics.

Future growth will likely be concentrated in the Asia-Pacific region, where government incentives and a growing pool of scientific talent are attracting significant foreign investment. Analysts predict that the "hybrid" model of outsourcing—where companies use a mix of full-service partnerships and functional service provision (FSP)—will become the dominant strategy. This flexibility will allow pharmaceutical firms to navigate future global crises or supply chain disruptions with greater resilience. Ultimately, the market is evolving into a deeply integrated global network that prioritizes patient outcomes through collaborative, high-tech innovation.

FAQ: What is the forecasted size of the market by 2035? Ans: Some industry reports project the market to reach approximately $182.9 billion by 2035, growing at a steady annual rate.

https://www.marketresearchfuture.com/reports/biotechnology-pharmaceutical-services-outsources-market-12369Strategic Projections for the Biotechnology Pharmaceutical Services Outsourced Market Projections As we look toward the next decade, the outlook for the pharmaceutical services sector remains exceptionally bullish. The Biotechnology Pharmaceutical Services Outsourced Market Projections indicate that the global market value could surpass $180 billion by 2035. This long-term growth is expected to be sustained by the continuous entry of innovative biotech startups that lack in-house manufacturing capabilities. The rise of biosimilars is also projected to be a major revenue driver, as the healthcare industry seeks more affordable alternatives to expensive branded biologics. Future growth will likely be concentrated in the Asia-Pacific region, where government incentives and a growing pool of scientific talent are attracting significant foreign investment. Analysts predict that the "hybrid" model of outsourcing—where companies use a mix of full-service partnerships and functional service provision (FSP)—will become the dominant strategy. This flexibility will allow pharmaceutical firms to navigate future global crises or supply chain disruptions with greater resilience. Ultimately, the market is evolving into a deeply integrated global network that prioritizes patient outcomes through collaborative, high-tech innovation. FAQ: What is the forecasted size of the market by 2035? Ans: Some industry reports project the market to reach approximately $182.9 billion by 2035, growing at a steady annual rate. https://www.marketresearchfuture.com/reports/biotechnology-pharmaceutical-services-outsources-market-123690 Kommentarer ·0 Delinger ·210 Visninger ·0 Omtaler -

Leveraging Chronic Inflammatory Demyelinating Polyneuropathy Market Data for Clinical Success

In the age of big data, the ability to collect and analyze real-world evidence (RWE) is becoming a competitive advantage for pharmaceutical companies. By tracking how thousands of patients respond to specific dosages in a non-controlled environment, researchers can refine treatment protocols and identify sub-populations that may require more aggressive therapy. Electronic Health Records (EHR) and patient registries are providing a wealth of information regarding the long-term safety profile of immunoglobulins, which is essential for maintaining regulatory compliance and securing favorable reimbursement terms from insurance providers.

Utilizing Chronic Inflammatory Demyelinating Polyneuropathy Market Data allows stakeholders to predict supply chain needs with much greater accuracy. Since plasma-based products have long production lead times (often up to 12 months), predictive analytics are vital for preventing stockouts that could endanger patient health. Furthermore, data-driven insights are helping clinicians move toward a "proactive" rather than "reactive" treatment model, where therapy is adjusted based on early physiological markers rather than waiting for physical symptoms to worsen.

https://www.marketresearchfuture.com/reports/chronic-inflammatory-demyelinating-polyneuropathy-market-6947

FAQ: What is "Real-World Evidence" (RWE) in the context of CIDP? Ans: RWE refers to data collected regarding patient health status and the delivery of healthcare outside of traditional highly controlled clinical trials, such as from medical records or insurance claims.Leveraging Chronic Inflammatory Demyelinating Polyneuropathy Market Data for Clinical Success In the age of big data, the ability to collect and analyze real-world evidence (RWE) is becoming a competitive advantage for pharmaceutical companies. By tracking how thousands of patients respond to specific dosages in a non-controlled environment, researchers can refine treatment protocols and identify sub-populations that may require more aggressive therapy. Electronic Health Records (EHR) and patient registries are providing a wealth of information regarding the long-term safety profile of immunoglobulins, which is essential for maintaining regulatory compliance and securing favorable reimbursement terms from insurance providers. Utilizing Chronic Inflammatory Demyelinating Polyneuropathy Market Data allows stakeholders to predict supply chain needs with much greater accuracy. Since plasma-based products have long production lead times (often up to 12 months), predictive analytics are vital for preventing stockouts that could endanger patient health. Furthermore, data-driven insights are helping clinicians move toward a "proactive" rather than "reactive" treatment model, where therapy is adjusted based on early physiological markers rather than waiting for physical symptoms to worsen. https://www.marketresearchfuture.com/reports/chronic-inflammatory-demyelinating-polyneuropathy-market-6947 FAQ: What is "Real-World Evidence" (RWE) in the context of CIDP? Ans: RWE refers to data collected regarding patient health status and the delivery of healthcare outside of traditional highly controlled clinical trials, such as from medical records or insurance claims.0 Kommentarer ·0 Delinger ·211 Visninger ·0 Omtaler

Flere historier