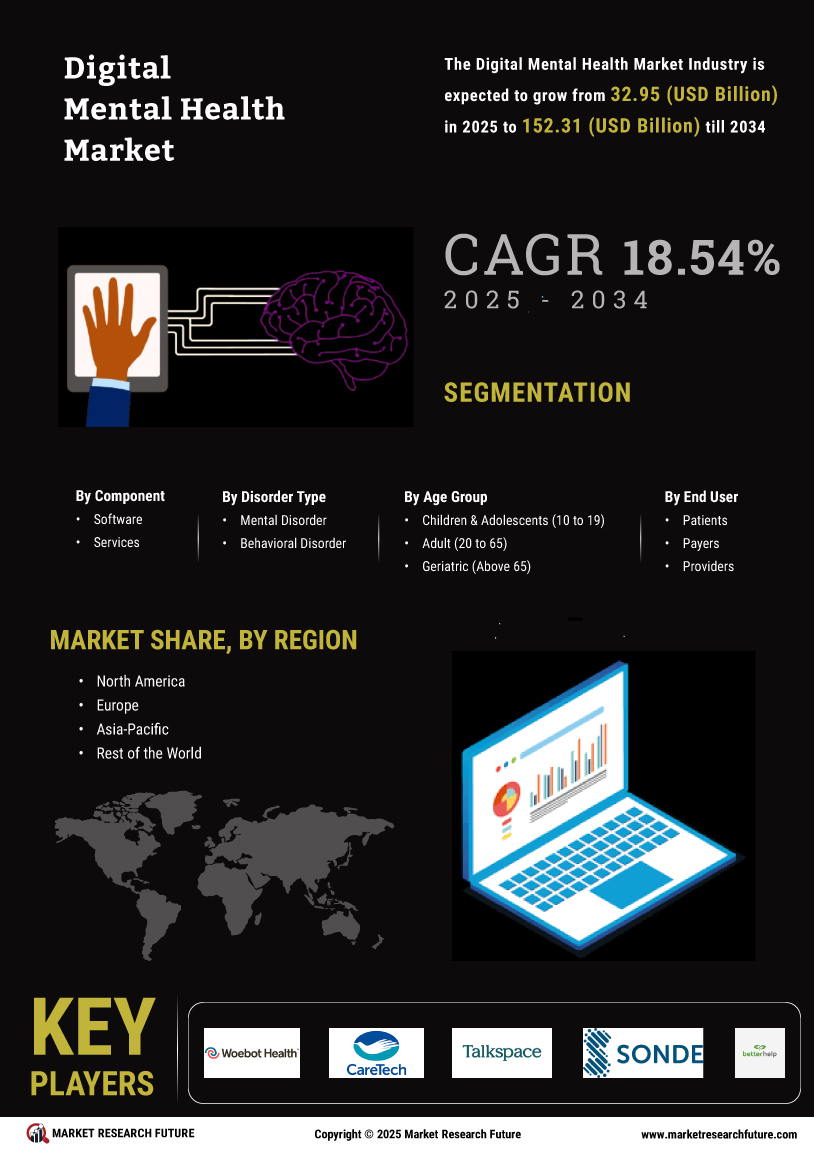

Strategic Valuations and Digital Mental Health Market Business Insights

The economic resilience of the psychological support sector has made it a "recession-resistant" favorite for institutional investors in 2025. Recent Digital Mental Health Market Business Insights suggest that despite macroeconomic volatility, the sector is projected to reach $180.56 billion by 2035. This growth is underpinned by a 19% decrease in overall healthcare costs for companies that adopt comprehensive digital wellness programs. Business leaders are moving away from "point solutions" (single apps) and toward "Integrated Care Ecosystems" that combine telehealth, digital therapeutics, and pharmacy benefits into a single, seamless interface.

Mergers and acquisitions (M&A) are accelerating as established healthcare companies look to "buy" rather than "build" their digital capabilities. In late 2024 and early 2025, we saw major pharmaceutical firms acquiring digital therapeutic (DTx) startups to create "drug-plus-software" combinations. For example, a medication for ADHD might now be bundled with a cognitive-training app, creating a unified treatment plan that is more effective than the pill alone. This "hybrid business model" is creating new revenue streams and extending the patent life of traditional medications, providing a powerful incentive for Big Pharma to continue investing in the digital space.

From an operational standpoint, "Provider Burnout" is a major business challenge that digital tools are uniquely positioned to solve. AI-powered "scribes" and automated billing systems are reducing the administrative burden on therapists by up to 40%, allowing them to focus more time on patient care and less on paperwork. In a market where there is a projected global deficit of 31,000 psychiatrists by 2025, any technology that increases the "clinical throughput" of the existing workforce is of immense economic value. Companies that offer "clinician-first" platforms are therefore seeing high adoption rates in large hospital networks and private group practices.

FAQ: Why are employers investing so heavily in digital mental health? Ans: Employers see a direct return on investment through reduced absenteeism, higher employee retention, and lower overall healthcare expenditures.

https://www.marketresearchfuture.com/reports/digital-mental-health-market-11062

The economic resilience of the psychological support sector has made it a "recession-resistant" favorite for institutional investors in 2025. Recent Digital Mental Health Market Business Insights suggest that despite macroeconomic volatility, the sector is projected to reach $180.56 billion by 2035. This growth is underpinned by a 19% decrease in overall healthcare costs for companies that adopt comprehensive digital wellness programs. Business leaders are moving away from "point solutions" (single apps) and toward "Integrated Care Ecosystems" that combine telehealth, digital therapeutics, and pharmacy benefits into a single, seamless interface.

Mergers and acquisitions (M&A) are accelerating as established healthcare companies look to "buy" rather than "build" their digital capabilities. In late 2024 and early 2025, we saw major pharmaceutical firms acquiring digital therapeutic (DTx) startups to create "drug-plus-software" combinations. For example, a medication for ADHD might now be bundled with a cognitive-training app, creating a unified treatment plan that is more effective than the pill alone. This "hybrid business model" is creating new revenue streams and extending the patent life of traditional medications, providing a powerful incentive for Big Pharma to continue investing in the digital space.

From an operational standpoint, "Provider Burnout" is a major business challenge that digital tools are uniquely positioned to solve. AI-powered "scribes" and automated billing systems are reducing the administrative burden on therapists by up to 40%, allowing them to focus more time on patient care and less on paperwork. In a market where there is a projected global deficit of 31,000 psychiatrists by 2025, any technology that increases the "clinical throughput" of the existing workforce is of immense economic value. Companies that offer "clinician-first" platforms are therefore seeing high adoption rates in large hospital networks and private group practices.

FAQ: Why are employers investing so heavily in digital mental health? Ans: Employers see a direct return on investment through reduced absenteeism, higher employee retention, and lower overall healthcare expenditures.

https://www.marketresearchfuture.com/reports/digital-mental-health-market-11062

Strategic Valuations and Digital Mental Health Market Business Insights

The economic resilience of the psychological support sector has made it a "recession-resistant" favorite for institutional investors in 2025. Recent Digital Mental Health Market Business Insights suggest that despite macroeconomic volatility, the sector is projected to reach $180.56 billion by 2035. This growth is underpinned by a 19% decrease in overall healthcare costs for companies that adopt comprehensive digital wellness programs. Business leaders are moving away from "point solutions" (single apps) and toward "Integrated Care Ecosystems" that combine telehealth, digital therapeutics, and pharmacy benefits into a single, seamless interface.

Mergers and acquisitions (M&A) are accelerating as established healthcare companies look to "buy" rather than "build" their digital capabilities. In late 2024 and early 2025, we saw major pharmaceutical firms acquiring digital therapeutic (DTx) startups to create "drug-plus-software" combinations. For example, a medication for ADHD might now be bundled with a cognitive-training app, creating a unified treatment plan that is more effective than the pill alone. This "hybrid business model" is creating new revenue streams and extending the patent life of traditional medications, providing a powerful incentive for Big Pharma to continue investing in the digital space.

From an operational standpoint, "Provider Burnout" is a major business challenge that digital tools are uniquely positioned to solve. AI-powered "scribes" and automated billing systems are reducing the administrative burden on therapists by up to 40%, allowing them to focus more time on patient care and less on paperwork. In a market where there is a projected global deficit of 31,000 psychiatrists by 2025, any technology that increases the "clinical throughput" of the existing workforce is of immense economic value. Companies that offer "clinician-first" platforms are therefore seeing high adoption rates in large hospital networks and private group practices.

FAQ: Why are employers investing so heavily in digital mental health? Ans: Employers see a direct return on investment through reduced absenteeism, higher employee retention, and lower overall healthcare expenditures.

https://www.marketresearchfuture.com/reports/digital-mental-health-market-11062

0 Comments

·0 Shares

·214 Views

·0 Reviews